Publicité

Fit and Proper Person : how Rigid is Banking Recruitment?

Publié le:

17 October 2018 à 07:37

The banking sector is considered as the driving force for our growth. With recent confusions, nominations and resignation, questions arise whether the Fit and Proper Person Criteria, as set by the Bank of Mauritius, are being used in reality. To what extent do these criteria form an integral part before any recruitment?

The recent confusion about the appointment of the CEO of MauBank, Anoop Nilamber, raises several questions about the Fit and Proper Criteria. What is it all about? How far is this fundamental criteria being used? Competency, honesty, financially sound: These are the predominant requirements established by the Bank of Mauritius for the probity and competence of senior officers, directors and shareholders who exercise significant influence on financial institutions.

In its Guideline on Fit and Proper Person Criteria, the Bank of Mauritius (BOM) clearly underlines that a person is considered to be ‘fit and proper’ if he is essentially of good character, competent, honest, financially sound, reliable and discharges and is likely to discharge his or her responsibility fairly.

This guideline is applicable to banks, non-bank deposit taking institutions, foreign exchange dealers and money changers, collectively referred to as financial institutions or institutions. The guideline recalls that the criteria are to be applied individually but it is their cumulative effect, which will determine whether a person meets the test. Nevertheless, the guideline affirms that a failure to meet one criterion does not necessarily mean failure to meet the test of ‘fit and proper person’. “The process will involve a good measure of judgment, which must be exercised in a fair and judicious manner, always in the best interests of the institution and the sound conduct of its business. The application of fitness and probity tests may vary depending on the degree of a person’s influence and on the person’s responsibilities in the affairs of the financial institution.”

As defined by the guideline of the BOM, Fit and Proper means a person who can discharge his responsibilities in a competent, honest and correct manner in the best interests of the institution.

Usually, the fit and proper is mostly used for senior officers of financial institution such as the Chief Executive Officer, Deputy Chief Executive Officer, Chief Operating Officer, Chief Financial Officer, Secretary, Treasurer, Chief Internal Auditor or Manager of a significant business unit.

According to the BOM, it is up to the board of directors of any financial institution to establish fit and proper person policy, taking into consideration the guideline emitted by the BOM. The board of directors has also the responsibility in ensuring proper documentation before a decision is reached. “The board’s further responsibilities are to ensure that nominations, initiated by the Board, of persons for election to the board of directors meet the test of fit and proper person set out in the Guideline before such nominations are placed before the shareholders’ meeting.”

According to the BOM guidelines, it is the responsibility of senior officers to show that they are fit and proper. Hence, they are called to complete the Fit and Proper Person Questionnaire as well as provide additional information required. However, the officers are obliged to “notify the board forthwith of any events or circumstances that have occurred subsequent to their initial assessment of fit and proper person that might change the assessment or at least have a material bearing on it.”

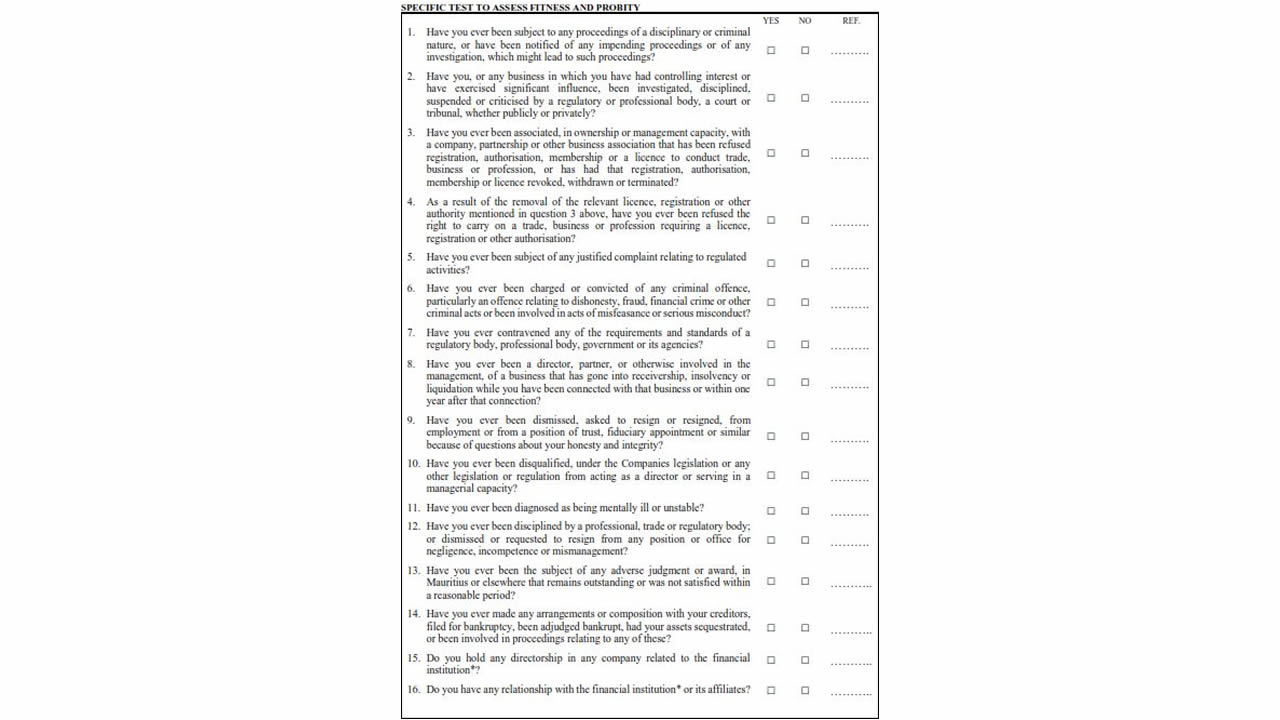

There are three main criteria to assess fitness and probity of a person:

In order to determine, a person’s honesty, integrity, diligence, reputation and good character, the board of directors needs to consider various components. For instance, it is necessary to check whether the person has been subject to any proceedings of a disciplinary or criminal nature or if there are any impending proceedings. Another element to be checked upon is whether the individual has been engaged in any deceitful business practices or is associated with a company, partnership or other business association or has been a director, partner, or otherwise involved in the management, of a business that has gone into receivership, insolvency, or liquidation.

Concerning competence and capability, it is mentioned that the board of directors must ensure that the person appointed must demonstrate qualifications and experience required as well to see whether the person has ever been diagnosed with mental illness. It is also the responsibility for the board to check for any mismanagement, incompetency or negligence.

As for the third criteria, it is essential for the officer to show that he has been able to manage his own financial affairs appropriately. The guideline maintains that in a situation whereby “a person has failed to manage his or her debts or financial affairs satisfactorily, especially where a loss was caused to others, the person’s competence, honesty and integrity may be in doubt.”

Corporate lawyer Sunil Bheeroo provides a better insight on the test of fit and proper criteria putting much emphasis on its importance and how it ensures integrity and honesty.

Why is Fit and Proper criteria important in the banking sector?

The banking sector is one of the most important sectors and of fundamental importance in our economy. Therefore, those who are recruited to work therein must be fit and proper in as much as they would be called upon to manage their respective institution and discharge their duties competently, professionally and honestly without any potential risk of fraud and significant ‘fault’.

Banking institutions are governed by the Banking Act 2004 as amended and the Central Bank is the regulator. The Central Bank of Mauritius which is governed by the Central Bank of Mauritius Act was established by the then Prime Minister Sir Seewoosagur Ramgoolam where Monetary policies was entrusted upon. The Bank of Mauritius was also established by legislation which has been amended from time to time, establishing the criteria as to whom would be a fit and proper person for senior positions and responsibilities thereof. The guidelines of the BOM emphasize this further.

How would you define a fit and proper person?

By definition, ‘fit and proper’ means a person who when subjected to the criteria of the guidelines together with any other criteria prescribed by the board of directors, presents the likelihood of them being in a position to discharge their responsibility in a competent, honest and correct manner in the best interest of the institution. The ‘fit and proper’ principle has established itself as a gatekeeping function for banks and financial institutions, where decisions taken impact a wider array of bodies, institutions and even individuals.

Usually, there would be an in-depth scrutiny into the individual’s profile, a questionnaire devised by the Bank, to start with, followed by further assessments of the individuals’ credentials.

Do you believe these criteria should be applicable for all employees in the banking sector?

Presently, it is applicable to senior officers such as the C-Suite along with those holding positions of high responsibility and confidentiality such as; the Treasurer, the Chief Internal Auditor and even Managers of relevant departments. In my humble opinion, a review of the current BoM guidelines with a view of revisiting their scope and objectives is well due in order for us as an economy to remain paced with the current times. Given that the banking sector is the pinnacle in a developing economy, the remit of the criteria of being a ‘fit and proper’ while exercising in the banking sector will not only enhance accountability but will also help improve productivity given the increasingly demanding political and economic arena.

In our current economic state, we cannot afford having officers with dubious risk profiles operating at the forefront of our banking sector, irrespective of the degree of potential risk. Hence the need for a review, and in so doing, political nominees would also be subject to the assessment of being fit and proper prior to assuming responsibility, instead of being imposed upon the operations of financial institution and opening up a consequential snowball effect of poor judgments, unsound decisions and reprehensible behavior.

How does this procedure ensure integrity and honesty?

The procedure is prescribed in the law and embedded in the guidelines of BoM whereby the candidate is called upon to answer all the questions in relation to their competency, honesty and integrity. Upon completion of the said questionnaire, an assessment is made as to whether the candidate has passed the test and could be therefore a probable officer in position of seniority. The onus is on the candidate to demonstrate they qualify as a ‘fit and proper person’.

An individual who fills out the questionnaire and fails to disclose material facts, which are later discovered by the regulator, is inevitably disqualified from fulfilling the responsibilities of the position they are entrusted with. The recent case of MauBank is a contemporaneous example of the trustworthiness of the ‘fit and proper’ concept, which further proves the need for the scrutiny to instill confidence in the clients of a bank or financial institution.

What, do you think, should be done to promote the use of these criteria?

The criteria are well established already but need to be revisited so as to amplify the scope of the scrutiny to include any recruits in banking and financial institutions as a whole. At the time of its establishment in 1967, the Minister of Finance sought to inculcate trust and belief that the Central Bank and its culture would mold financial and banking transactions for the welfare of the economy and state; “The time, however, had come for a rather more modern and sophisticated organization to look after the broader technical aspect of our monetary affairs.” It is now high time for a review so that Mauritius can be placed as a model amongst other nations and be competitive with the rest of the developing countries. Today we have a large number of banks operating on the island whether retail, corporate, investment, private banking, among others, which are promoting the development of the country and securing a spot in the global financial market but in order to project the right image for the financial industry, transparency, accountability and meritocracy must retain fundamental importance.

The former Governor of the Bank of Mauritius states that the banking sector is based on trust and hence the test of fit and proper is of utmost importance. “While filling in for information, the candidate should not hide any information. Besides, if there is any element of doubt, there is need for further investigations. It is all a question of trust.”

He maintains that it is important for a financial institution to have trustworthy people to maintain trust. “For the time being, seniors are subjected to these tests. But I truly believe that it should be from top to bottom including board directors. This will ensure that trust is maintained throughout the institution.”

Additionally, he states that even for political nominations, investigations should be carried out before any appointment. “The reputation of the bank matters more than anything. So, there is need to have people of trust working. There should be no cover ups and there should be no yes-man.”

The Bank of France made it clear that Anoop Nilamber does not face any bank bans or bad checks issue. He had applied for a right of access from the Bank of France for information on his banking history. Accordingly, the Bank of France informed the CEO in waiting of the MauBank that there is no information recorded in the Central Check File concerning the following charges: Incident of payment on checks for default or insufficiency of provision, forbidden to issue checks, Bank card withdrawal for misuse. Another clearance obtained by Anoop Nilamber is that he does not appear in the National Register of Personal Credit Reimbursement Incidents (FICP).

J'aime

J'aime