Publicité

Decline in Savings : are we becoming a nation of spendthrifts?

Publié le:

20 May 2019 à 06:54

Saving is key for a society to adequately provide for its future. According to the recent IMF Report Staff Report for The 2019 Article Iv Consultation, the private saving rate in Mauritius has been declining for years, contributing to a lower national saving rate and a sizable current account deficit. Why is such a situation prevailing? What could this decline in savings lead to? Experts in the finance and banking sector voice their concerns about this alarming situation.

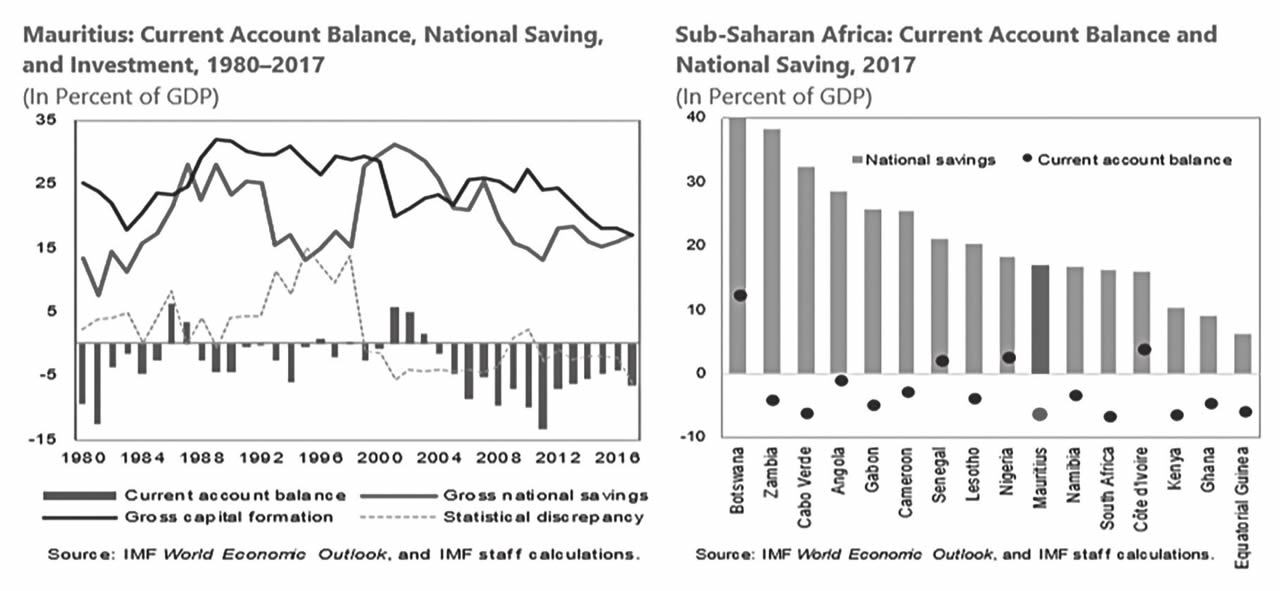

The IMF report shows that over the last four decades, the deposit rate and economic growth are the key drivers of private savings in Mauritius. Given the economic and demographic characteristics, private saving rate is about 3 percent of GDP lower than the potential in Mauritius. The report highlights that the current account balance of Mauritius has been in a persistent deficit since the mid-2000s, peaking at about 10 percent of GDP in 2010. “From a savings and investment perspective, Mauritius’ current account deficit can be largely attributed to a decline in national savings, as investment has remained tepid. National savings fell sharply during the global financial crisis in 2008–09, but recovered somewhat in 2011, and have averaged about 17 percent of GDP since then.”

Tahir Wahab explains that savings rate is the amount of money, expressed as a percentage or ratio that a person deducts from his disposable personal income to set aside as a nest egg or for retirement. The cash accumulated is typically put into very low-risk investments like savings accounts, fixed deposits and retirement scheme plan.

According to him, with globalisation and online purchase, consumers are now able to enjoy a wider variety of goods that were not previously available. “The marginal fall in the saving rate, therefore, reflects on an increase in consumption. Additionally, the influence of credit system of business contributes to a huge extent and people ‘spend first and then save’ whereas the principle should have been ‘save first and spend’. Globalization has inculcated a feeling of ‘living now’ instead of ‘living later’ more than ever and people believe more in instant gratification than delayed gratification.”

Sanjay Matadeen, Economist and Senior Lecturer, Middlesex University Mauritius Branch Campus, reveals that the fall in private saving rate in Mauritius over the years can be explained by rising consumption expenditure, rising household debts and macroeconomic conditions prevailing in the country namely in terms of low inflation and rising imports. “Mauritius has become a high consumption economy, in terms of increased expenditure on durable goods and non-durable goods. A lot of this consumption is financed through hire purchase and bank credit which have become relatively cheaper in a low inflation economy. The level of household debts has soared for many Mauritians.”

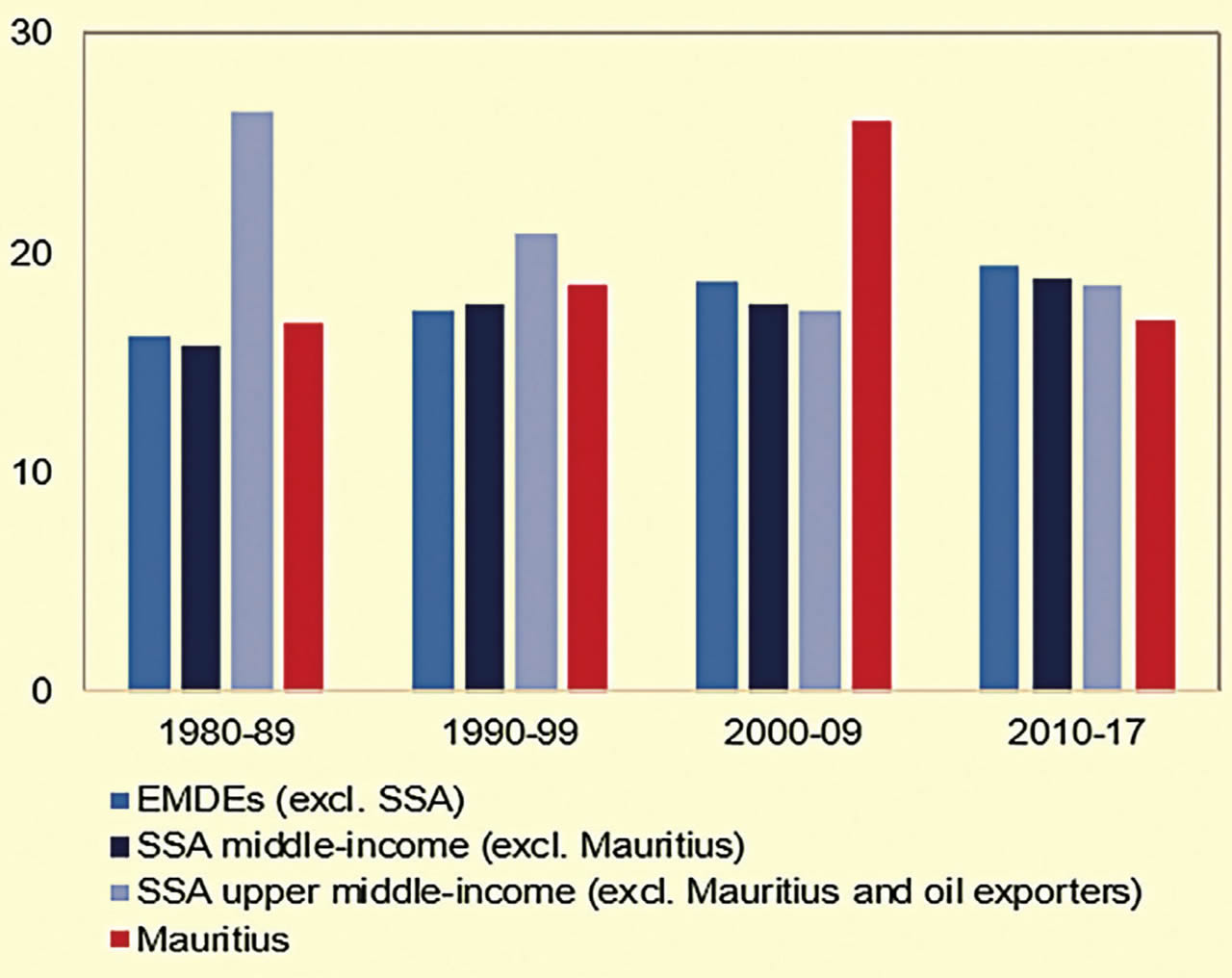

The Founder and Head of Programme of the New Economic Thinking Academy, Amit Achameesing, states that a major factor is the dynamics of income inequality in Mauritius. “As from 2000, the Gini index shows that inequality has consistently worsened up to 2016. As a consumer driven economy, this rising inequality due to stagnant real incomes of low and middle income households, has led to more borrowing to finance consumption and housing resulting in a lower private savings rate. Indeed, during the past two decades, there has been a rise in total household credit from 11% of GDP to 23% of GDP and a decline in the savings rate from 32% to 19% of GDP.”

While observing the trend of saving, the question that crops up is: Are we becoming a nation of spendthrifts? Why are Mauritians losing interest in saving? To this pertinent question, Tahir Wahab confides that the “majority of the population doesn’t have a savings capacity at the end of the month; the reasons are numerous. During recent years, the sharp increase in housing loans and consumption credit have led Mauritians into a debt spiral and constantly living beyond their means. Secondly, low income-earners spending the majority of their money on basic necessities rather than thinking to save for the future, as they are struggling to meet the ends. Thirdly, the low rate of interest on savings accounts in banks is another factor which does not make savings attractive enough.”

For Amit Achameesing, it is not a question of whether Mauritians are interested in savings but rather about their ability and willingness to save. “It is important to mention that the real interest rate has also been on a long-term downward trend. Today, the savings rate is barely 2% per annum while the inflation rate is around 3.5% per annum, which means that we currently have a negative real savings rate of 1.5%.”

If the same situation persists, it will have serious implications and consequences in our country. Sanjay Matadeen is of the view that in the short term, a fall in savings is not necessarily bad as an increase in consumption tends to give a boost to the economy and has multiplier effects but in the longer term, lower savings will mean that money creation in the economy will fall, thereby negatively impacting future investment and economic growth. “Savings is deferred consumption, and if savings falls, it will mean consumption and growth in the future will be affected.”

Similarly, Tahir Wahab argues that a lower saving ratio also has an impact on the long-term performance of the economy. “Lower savings means banks have a lower level of funds to finance investment. If the declining trend of household savings continues and being reliant on low savings and high consumer spending to sustain economic growth may pose some challenge to GDP growth and macroeconomic stability. A low domestic savings rate has the potential to lock a country into a permanently lower growth path as low savings levels lead to a lack of investment and, eventually, a lack of innovation or technological change, which is necessary for permanently higher growth rates.”

Moreover, the report maintains that as in other countries in SSA, national savings in Mauritius are mainly driven by private savings, which have fallen from a peak of 32 percent of GDP in the early 2000s to about 18 percent of GDP over the last decade. “This rate is lower than the average private saving rate for other emerging markets and developing countries (EMDEs).”

The report adds that “a rapidly rising old-age dependency ratio requires a higher level of savings to alleviate fiscal pressures and avoid abrupt policy adjustments in the future. In this regard, efforts should focus on generating greater public awareness and encouraging private savings — for example, through old-age related saving schemes. Better targeting of social benefits and broader pension reforms could also help to boost savings.”

In the Annual Report and Audited Accounts 2017-18 of Bank of Mauritius, the Bank Governor, Yandraduth Googoolye, had remarked that the rise in the short-term money market rates has resulted in a widening of the spread vis-à-vis savings deposit rates. He made an appeal upon banks to increase their savings deposit rates so that savers can benefit from a higher return. “Some banks have already increased their rates.”

In order to reverse the situation, various initiatives should be taken by the authorities. The various proposed incentives are as follows:

Tax incentives

Tahir Wahab states that “there should be tax incentive like in the past where people investing in a life insurance are able to claim tax deductions. This is a clear incentive on how to motivate and attract people to invest for the future.”

Financial literacy

Sanjay Mataden explains that the financial literacy of Mauritians should be improved with the right sensitization and training at school and community level. “How to draw a monthly budget can help Mauritians to plan their monthly expenditure, escape from rising debt and save for the future.” He also adds “there are also a number of informal ways beyond bank saving accounts for saving, for example savings club, Rotating Credit and Savings Associations (ROSCA’s) where people save together in a group and take turns to draw money and Credit Unions.”

Financial reforms

Amit Achameesing claims that there is need radical structural and financial reforms in order to bolster economic growth and permanently increase private savings. In a nutshell, the country needs to rewrite the rules of its economy for the 21st century.

Shehryar Bakht Ali : “Saving for the future is becoming a growing concern”

Shehryar Bakht Ali : “Saving for the future is becoming a growing concern” Head of Retail Banking, Bank One Limited Shehryar Bakht Ali believes that saving for the future is a key area of focus for Mauritians, however, the mode of savings or investments tool that customers choose to use may vary subject to the returns and demographic based preferences. “Since the benchmark interest rates have reduced during the past decade from 9.25% in 2007 to 3.5%, this has had a commensurate effect on customers finding other avenues to invest. Mauritians are generally concerned in saving for the future. Millennials are showing growing tendencies to save as they age through differentiated return/affinity driven savings and investment tools which talk to their values, needs and future aspirations.”

Dan Maraye : “It is high time for the authorities to come forward with incentives”

Dan Maraye : “It is high time for the authorities to come forward with incentives” Former Bank of Mauritius Governor Dan Maraye says that the Mauritian population is divided into diverse categories. “One category believes in saving; another category will not save while a third category is willing to save but is unable to do so. In order to be able to save, the individuals need to have a revenue. If a person does not have the revenue desired, then it will be impossible to have savings. A fourth category of people lives in debts.”

He further states that people are not interested in saving since they are unable to get what they desired as outcome. “If an individual is saving or investing in a scheme and not getting an interesting rate, he will be discouraged to continue. It is high time for the authorities to come forward with incentives to motivate people to invest. It is also important to educate children about saving as from school.”

J'aime

J'aime